Wealth Gap PLUS Debt Final

Acknowledgments

The author would like to thank the numerous researchers, experts, and practitioners who graciously shared their insights, knowledge, and experiences, and those who took the time to review an early draft of this paper: Carla Fletcher and Jeff Webster from Trellis Research, Kevin Fudge from American Student Assistance, Tiffany Jones from The Education Trust, and Ben Miller from the Center for American Progress. Thanks to Ā鶹¹ū¶³“«Ć½ colleagues Kevin Carey, Rachel Black, Kim Dancy, and Sabrina Detlaf for their expert and editorial insight. Maria Elkin and Riker Pasterkiewicz provided layout and communication support.

This work would not have been possible without the generous support of Lumina Foundation and the Bill & Melinda Gates Foundation. The views expressed in this paper are of the authors alone.

Downloads

Introduction

In the summer of 2012, America was still in recovery from the worst economic recession since the Great Depression. Congress and President Obama were focused on the impending election, a period that usually involves little in the way of controversial policymaking or change. But as the year drew to a close, something strange began happening with a U.S. Department of Education loan program known as Parent PLUS, under which parents borrow money from the government to finance their childrenās education (See Box 1: What Are Parent PLUS Loans?).

It started with whisperings among financial aid administrators that more parents were being rejected for the loan than usual. It seemed that at some point after students arrived for fall semester 2011, the Education Department began tightening the credit check criteria for PLUS loans. Rejections continued to swell through the spring and summer semesters. By the following autumn, some collegesāparticularly those that enroll many low-income minority studentsāwere in significant financial distress. Without access to PLUS loans, parents could not pay tuition bills.

Urgent calls were made to the Education Department, Congress, and the White House. It turns out that the Department had discovered an error in the way the credit check had been implemented. This error was discovered after the federal loan program transitioned to full direct lending in July 2010. Before then, the federal student loan program made loans under two different programs: the Direct Loan program, where loans are issued directly through the Education Department, and the Federal Family Education Loan (FFEL) program, where loans were issued by private lenders and backed by the government. For all intents and purposes, the terms and conditions of the loans were the same. But the Department discovered a discrepancy between how the FFEL program implemented the credit check versus how it was done under Direct Loans. The Department had been, by mistake, making loans to parents with a history of accounts charged off to bad debt and accounts in collections.1 Therefore, the Department had no choice but to reconcile the two credit checks.

The Department thought the impact would be minor for parents and colleges. It was wrong. The change pulled the curtain back on a group of colleges and universities that were heavily reliant on revenue from federal loans made to low-income families of color with bad credit.

Black parents, who were deeply impacted by the subprime mortgage crisis and higher unemployment rates compared to other groups, were particularly hard hit. At some historically Black colleges and universities (HBCUs), rejections were so significant that students could no longer enroll, leaving colleges scrambling to fill budgetary holes. Carlton Brown, then president of Clark Atlanta University, an HBCU, remarked in an Education Department hearing, āthe drastic decision to change the credit regulations controlling the Parent PLUS loans without effective evaluation of its impact nationally and specifically on HBCUs and without prior communication and input, has resulted in a tornadic effect through the denials of 400,000 Parent PLUS applications, 28,000 of those for students at HBCUs.ā2

Reeling from such a dramatic loss in revenue, HBCU leaders and the Congressional Black Caucus demanded the change be reversed. As a result of their pressure, the Education Department rewrote the rules to make it easier for low-income parents with bad credit to borrow. Money began flowing again.

But none of those actions changed the dire underlying financial circumstances of low-income Black families struggling to send their children to college. New analysis of Education Department data show just how risky PLUS loans are for these families. This analysis also shows that when parent loans and student loans are considered together, federal student loan policies are driving an intergenerational accumulation of debt that burden the neediest families.

There is, sadly, ample precedent for this. For decades, federal, state and local policies, whether intentionally or unintentionally, have been crafted in ways that promote the wealth and advancement of white families while shutting families of color out. Each new widening of the racial wealth gap makes it more likely that the next allegedly neutral or universal program will in fact make the gap wider still.

"When parent loans and student loans are considered together, federal student loan policies are driving an intergenerational accumulation of debt that burden the neediest families."

This is what has happened with the Parent PLUS program. Although technically any parent of a dependent student has access to Parent PLUS, these loans were created to give middle- and upper-income parents, who are predominantly white, access to fixed-rate lower-interest loans for expensive institutions. Originally, federal aid was targeted to low- and moderate-income students. But in 1978, middle- and upper-income families were faced with high interest rates and increasing tuition bills, and they wanted a piece of the financial aid pie. The passage of the Middle Income Student Assistance Act expanded low fixed-interest federal student loans to most families regardless of income.3 The PLUS loan program built on that expansion when it was created upon the reauthorization of the Higher Education Act in 1980.

But now, as the cost of college has increased enormously for everyone, financial aid has failed to keep pace, and stops way too short for the lowest-income families. Families of color, especially Black families, have seen their wealth wiped away through decades of discriminatory practices and policies including a housing crisis brought about in part by predatory lending practices.

Wealth goes beyond income. Policies that have promoted wealth accumulation for white families have resulted in their ability to pass on that wealth, from providing their children with down payments for housesāa step that unlocks community resources and high-quality school systemsāto funding their education.4 Black families have never been able to build the same wealth, even when investing in higher education meant to level the playing field. Instead of higher education achievement disrupting the intergenerational wealth deficit, overreliance on higher-education debt worsens it.

This report looks at the Parent PLUS loan program and how it exacerbates the racial wealth divide by promoting debt among low-income Black families. The report focuses on Black families because they experience a wider racial wealth divide, and there is alarming new evidence that they also have the worst student loan repayment outcomes of any racial or ethnic demographic.5 The first part of the report examines the demographics of Parent PLUS families using Education Department data. It looks at average intergenerational debt for those families who borrow using PLUS and student loans. This analysis reveals that low-income Black families are burdened with large intergenerational education debts compared to their white peers. The second part of this report focuses on the implications of the racial wealth gap and how policies like PLUS have widened it. It shows how the PLUS program has come roaring back to life after the credit check regulation was weakened.

"Black families have never been able to build the same wealth, even when investing in higher education meant to level the playing field."

Given the enormous collection powers of the federal government, the Parent PLUS loan is becoming predatory for Black PLUS borrowers who are more likely to be low-income and low-wealth, and who will likely struggle to repay. This report ends with 12 steps that can be taken to help prevent the predatory lending that discourages wealth building among Black families and to ensure that students of color have access to an affordable higher education.

Box 1

What are Parent PLUS Loans?

Federal Parent PLUS loans are offered to parents of dependent students to help send their children to college. Most students are considered dependent if they are under the age of 24. Often these loans come into play after a student has maximized all other sources of aid including grants, scholarships, and federal student loans and still faces a gap in covering expenses for the academic year. Unlike federal subsidized or unsubsidized loans, which have strict borrowing limits, parents are able to borrow up to the total cost of attendance (COA), which can include room and board, transportation, books and supplies, and other indirect expenses critical to academic success in addition to tuition and fees. As a result, parents can borrow a sizeable amount, one that far exceeds the strict borrowing caps that undergraduate students face. The PLUS loan has a higher interest rate (currently 7 percent) than undergraduate student loans (currently 4.5 percent), and comes with a higher origination fee.

In order to obtain a Parent PLUS loan, a parent must undergo an adverse credit history check. This is solely an eligibility check and is not strict underwriting, as a parent is either approved or not, rather than approved for a specified dollar amount. Prospective borrowers fail the credit check if they have one or more debts with a total combined outstanding balance greater than $2,085 (pegged to inflation starting in 2015), 90 or more days delinquent, charged off, or in collections in the past two years or if they have been the subject of a default determination, bankruptcy discharge, foreclosure, repossession, tax lien, wage garnishment, or federal student loan debt write-off in the past five years.6 The federal government does not take into account whether the parent has the ability to repay the loan. The absence of a credit history does not count as an adverse credit history.

If rejected for a PLUS loan, a parent can obtain an āendorserā who will agree to repay the loan if the parent cannot. The parent can also appeal the decision by providing the Education Department with documentation of extenuating circumstances.7 If the parent decides not to obtain an endorser or to appeal, the child can borrow more student loans up to the independent student limit, often an additional $4,000 to $5,000, depending on year of study.

Just like federal student loans, Parent PLUS are usually not dischargeable in bankruptcy and the government can collect on defaulted debt through various means including wage garnishment, Social Security garnishment, and seizure of tax refunds. Unlike federal student loans, Parent PLUS loans are not traditionally eligible for income-driven repayment (IDR) plans such as Pay as You Earn. In some cases, PLUS can be consolidated into a federal direct consolidation loan and this consolidation can be repaid with one antiquated IDR plan known as Income-Contingent Repayment.

Few data are available on PLUS loans. Default data are largely unavailable other than estimated lifetime default rates buried in the presidentās annual budget request. Currently, the Education Department calculates three-year cohort default rates (CDR) of every school that participates in the federal student loan program. If an institutionās CDR is too high, it may eventually lose eligibility to disburse federal aid, possibly causing the school to shutter. This is one of the only methods the government has to protect students and taxpayers from schools that have poor outcomes with student loans. Unfortunately, Parent PLUS loans are not included in CDR calculations, rendering them a no-strings-attached revenue source for colleges and universities.

For this reason, some colleges and universities fill gaps in financial aid with PLUS loansāsometimes to the tune of thousands of dollarsāin financial aid award letters, making it seem like students and parents owe nothing for the academic year when most of their federal aid takes the form of parent and student loans. For many institutions, Parent PLUS loans are like grants: they get the money from the federal government and the parent is on the hook to repay.

Citations

- This information was given during a public event at Ā鶹¹ū¶³“«Ć½ by Ben Miller when he was Manager of Research with Ā鶹¹ū¶³“«Ć½ās Education Policy Program. Miller was a former U.S. Department of Education official when the PLUS Loan credit change occurred. For more information see, āParent PLUS or Minus: Promoting Access or Putting Parents at Risk?ā PowerPoint presentation at Ā鶹¹ū¶³“«Ć½, Washington, DC, January 8, 2014.

- Carlton Brown, āNegotiated Rulemaking for Higher Education 2013ā (testimony given at the U.S. Department of Education Office of Postsecondary Education Public Hearing, Atlanta, GA, June 4, 2013).

- Angelica Cervantes, Marlena Cruesere, Robin McMillion, Carla McQueen, Matt Short, Matt Steiner, and Jeff Webster, Opening Doors to the Higher Education Act: Perspectives on the Higher Education Act 40 Years Later (Round Rock, TX: Texas Guaranteed Student Loan Corporation, 2005), .

- Darrick Hamilton, William Darity, Jr., Anne E. Price, Vishnu Shridharan, and Rebecca Tippett, Umbrellas Donāt Make It Rain: Why Studying and Working Hard Isnāt Enough for Black Americans (New York, NY: The New School, Duke Center for Social Equity, and Insight Center for Community and Economic Development: 2015).

- The data in Appendices A and B provide a full breakdown of this analysis among white, Black, Hispanic/Latino, and Asian American borrowers and undergraduates.

- Rachel Fishman, āEducation Department Publishes Final Rule on PLUS Loans,ā EdCentral (blog), Ā鶹¹ū¶³“«Ć½, October 22, 2014, source.

- Federal Student Aid (website), U.S. Department of Education, āDirect PLUS Loans and Adverse Credit,ā March 2015, .

Part I: Intergenerational Higher Education Debt

A key question is whether Parent PLUS borrowers are able to pay back their loans. Unfortunately, data on PLUS loans often go unreported or are not even collected. For this reason, little is known about Parent PLUS borrowers and their repayment outcomes. To better understand the demographics of Parent PLUS borrowers, Ā鶹¹ū¶³“«Ć½ analyzed Education Department survey data.1 This includes the National Postsecondary Student Aid Study (NPSAS), a representative survey of students eligible for federal financial aid who are at any point in their academic career, and the Beginning Postsecondary Students Longitudinal Study (BPS), which follows a cohort of students over time to understand their outcomes, starting with their first year of enrollment. The NPSAS survey is useful to understand demographics of the students whose parents borrow PLUS loans, and the BPS survey is useful for understanding characteristics and outcomes over time of students whose parents borrow PLUS loans.2

A Snapshot of PLUS Loan Families in 2011ā12

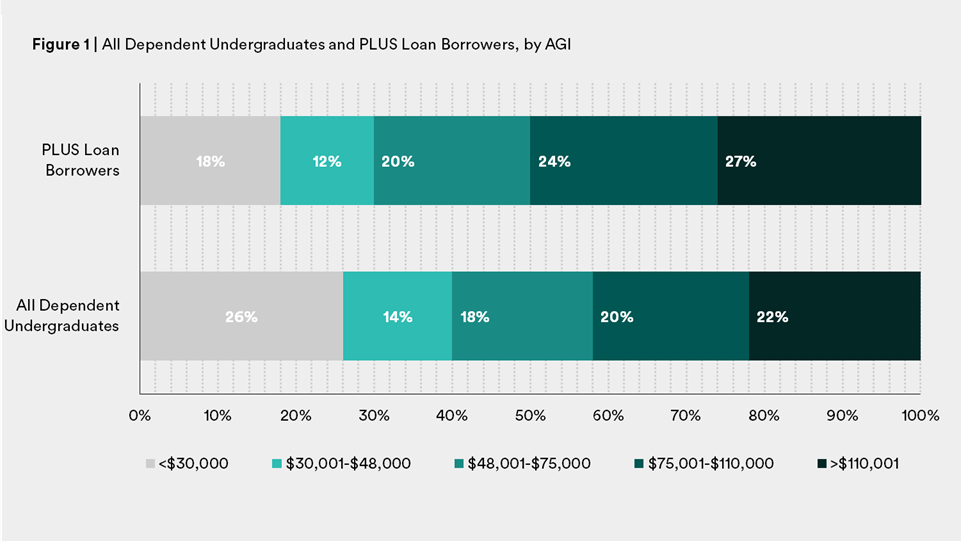

While only a small percentage of dependent students have parents who borrow PLUS loansāonly 5 percent in the 2011ā12 NPSASāwhen the data are analyzed by adjusted gross income (AGI), expected family contribution (EFC), and race/ethnicity, the findings are revealing. For comparison purposes, the data are presented next to that for all dependent undergraduates.

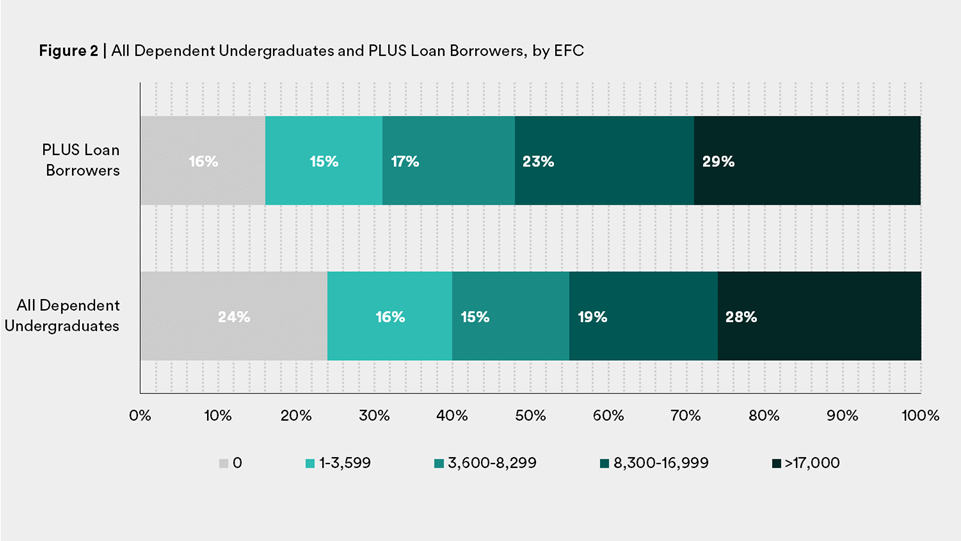

For those who have borrowed PLUS in 2011ā12, the data indicate that as AGI increases, so does the proportion of parents who borrow PLUS.3 (See Figure 1.) A majority of Parent PLUS borrowers come from families making more than $75,000. The program was designed to cater to these borrowers, giving middle- and upper-income borrowers access to a fixed-rate loan to pay for college. Looking at EFC, a measure established in law that tries to determine a familyās ability to pay for college and thus one that is correlated with income, shows largely the same story.4 (See Figure 2.)

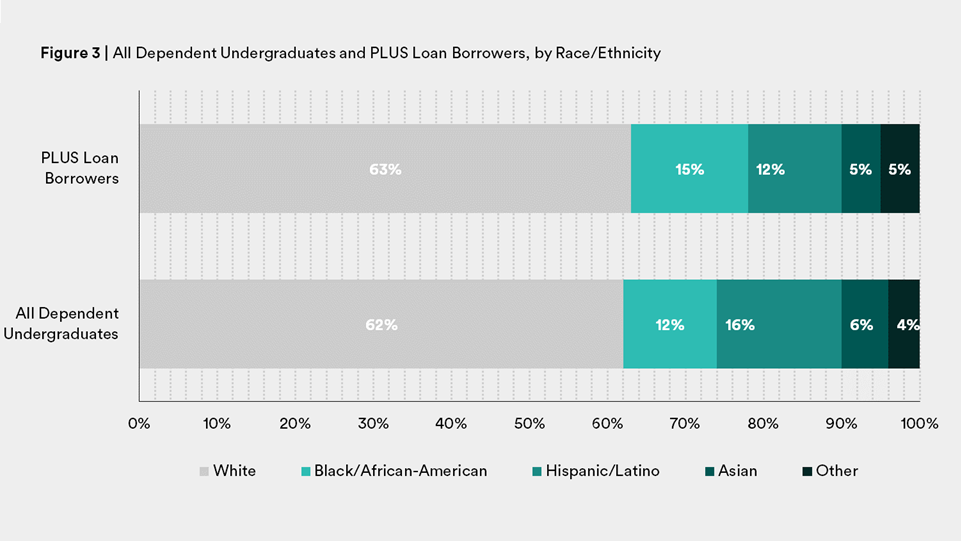

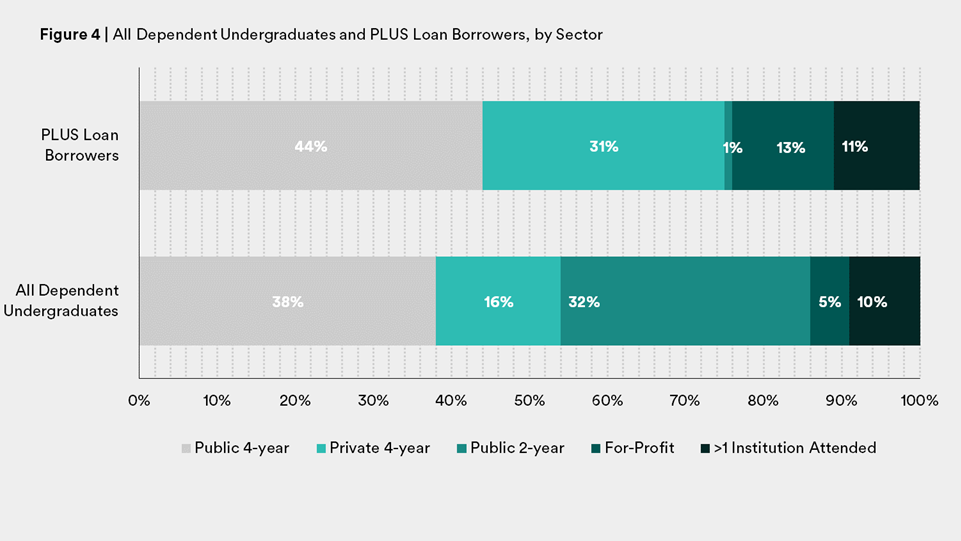

Most PLUS borrowers are white and have children who attend public four-year or private four-year institutions. (See Figures 3 and 4.)

In July 2015, when Martin OāMalley, former governor of Maryland, was running for president, he announced a plan for debt-free college. OāMalley used his own familyās scenario as reasoning for why a debt-free option was needed: for his two children he had borrowed $340,000 in PLUS loans.5 Like many PLUS loan borrowers, OāMalley is upper-income, white, and sent his children to expensive public (out of state) and private four-year institutions. While $340,000 may sound like a lot of debt for most familiesāindeed, it is more than median home prices in AmericaāOāMalleyās family is wealthy and can afford to repay the loan back.

For OāMalleyās family, higher-education debt is not a crisis in the way it is for other families. When looking at AGI and EFC by race it is clear that some low-income families of color are shouldering a lot of financial responsibility when it comes to sending their children to college.

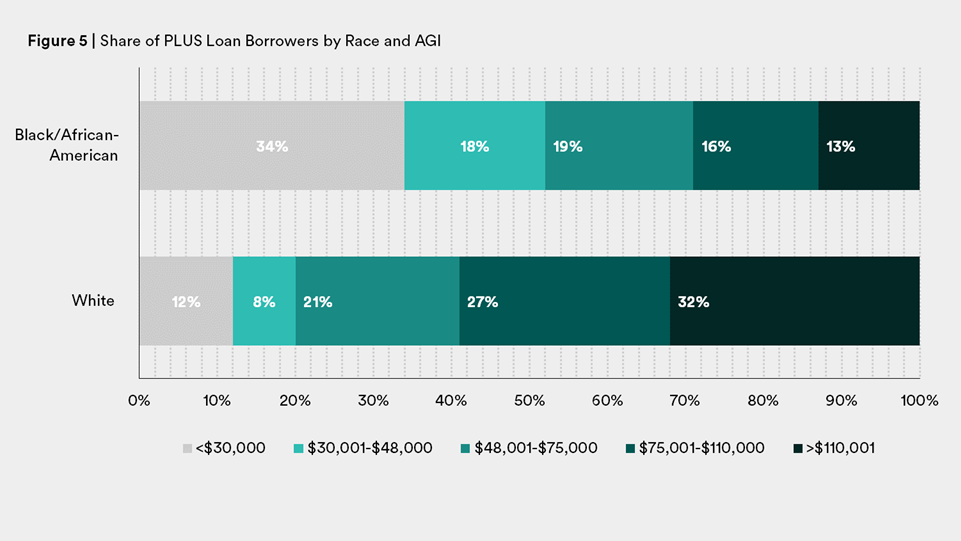

For white families, for the most part as income increases so does the share of PLUS borrowers. For Black families, it is exactly the opposite case. Approximately a third of white PLUS borrowers come from household AGIs of more than $110,001, with about one in 10 coming from families with AGIs less than $30,000. For Black families, about one in 10 have AGIs over $110,001, with approximately one-third having an AGI of less than $30,000. (See Figure 5.)

EFC largely follows the same pattern, with approximately one-tenth of white borrowers with an EFC of zero compared with a third of Black borrowers (See Figure 6). Arguably, no family with a zero EFC should take on a PLUS loan, as EFC is a rough approximation of the ability to repay a loan. The share of Black borrowers with zero EFC paints a stark picture of the inequity of debt burdens when it comes to paying for college.

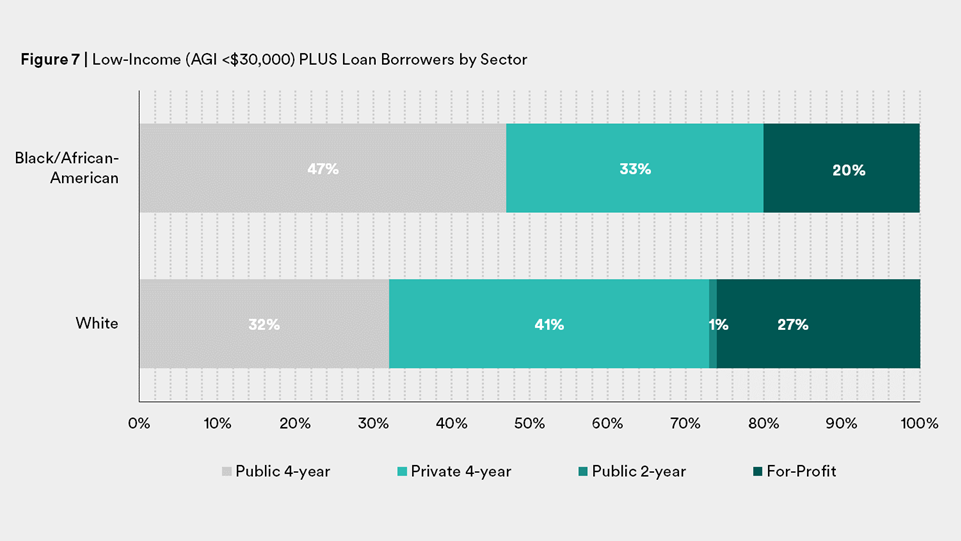

The types of colleges and universities where Black and white students enroll does not explain these patterns away. Low-income Black students whose parents borrowed PLUS are more likely to be enrolled in āaffordableā four-year public colleges and universities than more expensive private and for-profit institutions. The share of white low-income borrowers is actually comparatively higher in the private and for-profit sectors.6 (See Figure 7.)

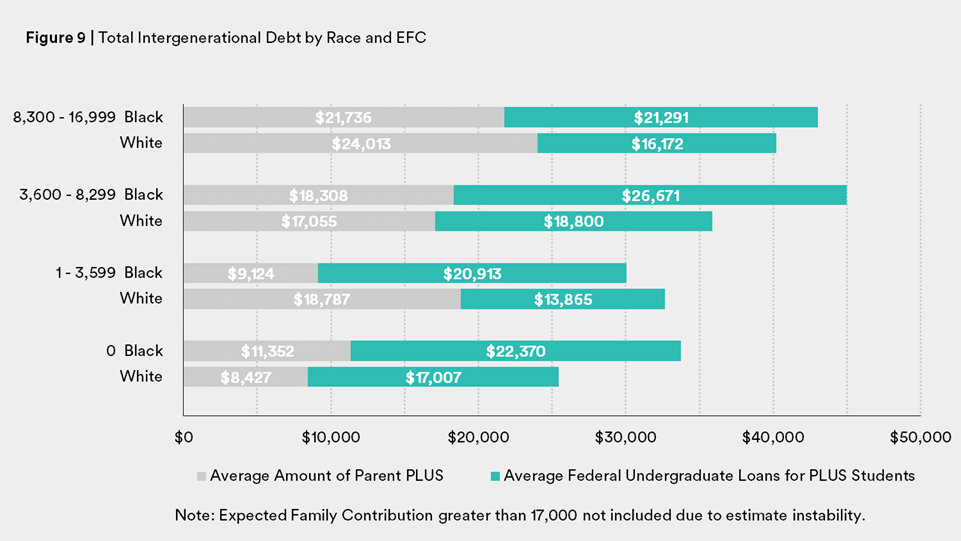

Total Intergenerational Indebtedness

Examining PLUS debt in isolation understates the true debt burden on low-income families. Parent PLUS loans are often borrowed only after students have borrowed the maximum amount of federal student loans, which can add up to $27,000 over four years in college. While hard data are unavailable to quantify this phenomenon, some parents may be taking out PLUS loans with the expectation that their children will be responsible for paying the loans back. The parents at the center of the PLUS controversy were, by definition, low-income borrowers with bad credit outcomes. Because college financial aid offer letters are often deliberately arcane and confusing, it may not be clear to parents and students whose debt is technically whose.7 In any event, the family as a whole is ultimately responsible for the combination of student and parent debt.

"Because college financial aid offer letters are often deliberately arcane and confusing, it may not be clear to parents and students whose debt is technically whose."

While NPSAS data give a snapshot of the demographics of borrowers during the 2011ā12 academic year, the BPS data set illuminates the demographics of PLUS borrowers and helps us understand average cumulative indebtedness over 12 years, from 2003ā04 to 2015ā16.

Often, media and policymakers focus on the debt burdens of graduating undergraduates or outlying graduate borrowers with six-figure debts. The Institution for College Access and Success, for example, publishes a widely-recognized and highly cited yearly report on the average debt for graduating bachelorās degree candidates.8 Yet for many families, a significant portion of debt in the form of parent loans goes unreported and uncalculated.

Approximately 16 percent of students who began their higher education in 2003ā04 had parents who borrowed a PLUS loan at some point by 2015ā16.9 Although only a relatively small subset of parents borrow, not including parental debt in total debt calculations understates higher-education debt. The average cumulative amount of PLUS loans over these 12 years was $20,343 per student whose parents borrowed PLUS.10 The average cumulative amount of undergraduate loan debt for these students was $17,307. This means that the average total intergenerational higher education debt for PLUS families, almost one in five dependent undergraduates, was nearly $38,000.

"A significant portion of debt in the form of parent loans goes unreported and uncalculated."

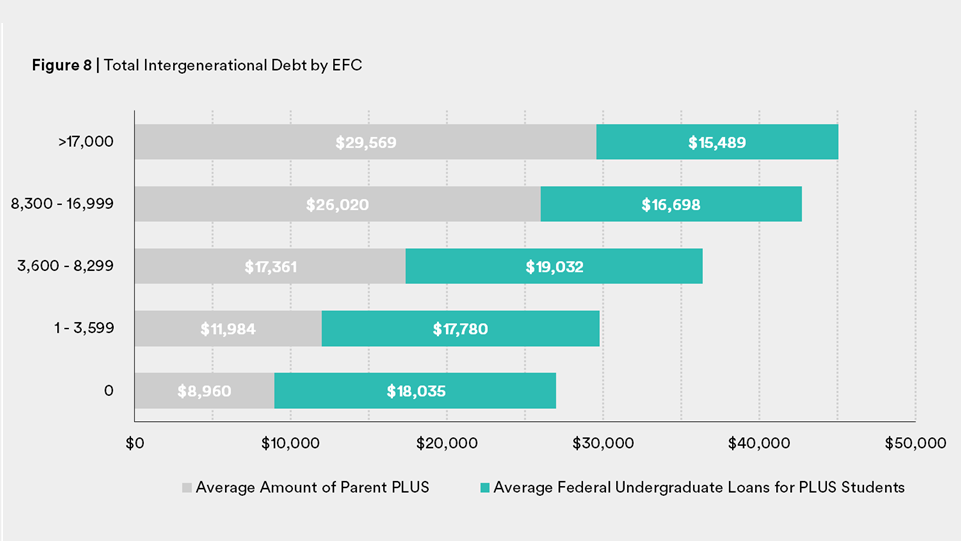

Like other patterns seen with PLUS loans, average intergenerational loan debt increases as EFC increases. The lowest-income familiesāthose who the federal government expect to contribute nothing to their cost of attendance because their need is so highāhave an average intergenerational debt of almost $27,000.

For white families who borrow PLUS and student loans, the average amount of cumulative debt increases as EFC increases (See Figure 9). For Black PLUS families, the story is different. Black families with zero EFC accumulated an average of $33,721 in intergenerational debt, of which $11,352 was in PLUS loans. By contrast, white families with zero EFC accumulated $25,434 in debt, 25 percent less. Even among families that the EFC formula judges equally needy, debt outcomes for white and Black families are very different. And unlike their white counterparts, the average indebtedness for Black families fluctuated as EFC increased, perhaps because even at similar income levels white and Black families have different levels of wealth.

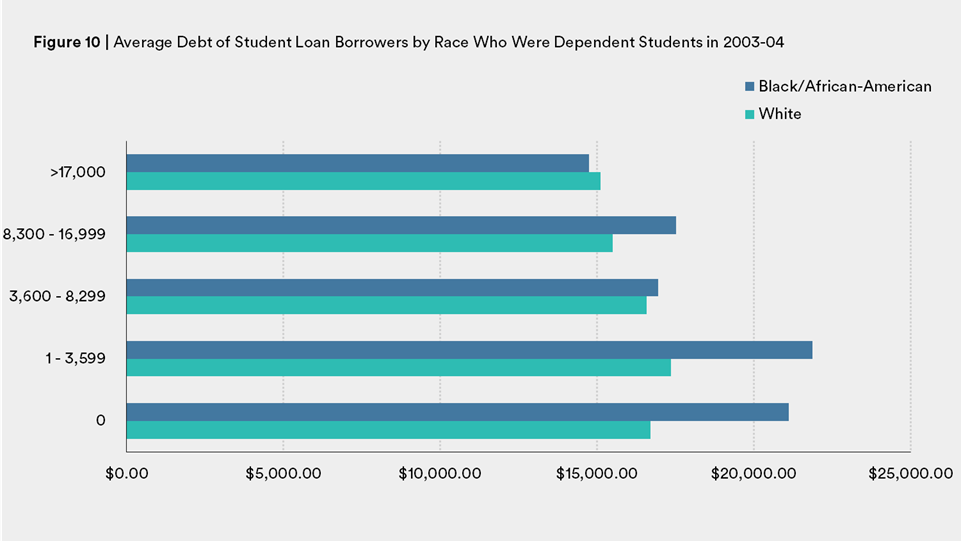

In comparison, dependent student loan borrowers whose parents did not borrow PLUS accumulated slightly less personal debt for their higher education. But low- and moderate-income Black borrowers still had borrowed much more than their white peers. (See Figure 10.)

Student Loan Debt Disparities

Unfortunately, practically nothing is known about Parent PLUS repayment outcomes. There is no consistent or good number on whether parents expect their own children to pay back this loan, how many parents are delinquent, how many are in default, and how many are experiencing the extreme pinch of government collection practices such as wage or Social Security garnishment and tax refund seizure. All there is to go by are repayment trends from undergraduate borrowers. And a growing body of work that looks at these outcomes reveals that Black undergraduates are experiencing a true student loan crisis. Given the disparity in borrowing PLUS loans and accumulating intergenerational debt, it may give hint of the burden Black families take on to get a higher education.

While it is clear from the Education Department survey data that low-income Black parents are borrowing PLUS loans at a higher rate than their low-income white counterparts, differences in debt accumulation do not stop there. Black students are more likely to borrow than their white, Asian, or Latino peers.

Overall, about one in four student loan borrowers is delinquent or in default.11 The previously mentioned BPS data set that followed a cohort of borrowers who entered higher education in 2003ā04 highlights problematic repayment trends, especially for Black borrowers. Ben Miller from the Center for American Progress found that 12 years after entering college, the median Black borrower owed more than the original amount borrowed.12 In other words, not only had Black borrowers at the median made no progress towards retiring their debt, their debt situation had actually worsened. This was not the case for median white and Latino borrowers, who had made progress in paying down their debt.13

What is even more worrisome is that a bachelorās degree, normally thought to protect borrowers in a bad labor market and help ensure they are able to repay their debts, does not insulate Black borrowers in the same way. While only 9 percent of borrowers with a bachelorās degree default on a student loan, the number jumps to one in four for Black borrowers.14

"Not only had Black borrowers at the median made no progress towards retiring their debt, their debt situation had actually worsened. This was not the case for median white and Latino borrowers, who had made progress in paying down their debt"

Not only are Black borrowers with bachelorās degrees less protected from repayment problems, for those who drop out the outlook is horrific, especially in the for-profit sector. Approximately three out of four Black students who attended for-profit institutions and dropped out went on to default on their loans.

Judith Scott-Clayton, in an analysis for the Brookings Institution, looked not only at the 2003ā04 cohort of borrowers, but also an earlier cohort who entered higher education in 1995ā96. By applying the trends of the earlier cohort to the later one, she finds that nearly two in five borrowers are projected to default on their loans by 2023.15 Like trends seen in Millerās analysis, Scott-Clayton finds that Black borrowers are especially vulnerable to delinquency and default. Black borrowers who earn a bachelorās degree are more likely to default than white borrowers who dropped out of college. She projects that approximately 70 percent of Black borrowers may end up in default.16

Yet even these sobering numbers do not include the additional burden of intergenerational debt and the repayment outcomes of various demographics of parent borrowers. It is hard to know for sure, but it is likely that repayment outcomes of student borrowers are correlated with parent repayment outcomes, especially given that some parents expect their children to repay PLUS loans. Given the debt crisis for Black student borrowers, there is likely a debt crisis for Black parent borrowers as well.

Box 2

Large Debt Burdens of Grad and Parent PLUS Loan Borrowers

Recently, Adam Looney from the Brookings Institute and Constantine Yannelis from New York University reviewed National Student Loan Data System (NSLDS) data and found that, increasingly, more higher education loan borrowers (17 percent) have debt balances over $50,000 and this debt accounts for the majority of federal higher education loan debt owed to the government.17 The growth in loan balances is partly explained through the growth of lending to graduate students through a program known as the Grad PLUS program, but Parent PLUS borrowers are also a driving factor.18

According to their analysis, in 2000, the share of Parent PLUS borrowers with debt over $50,000 was approximately 3 percent, but by 2014 the share was up to 13 percent. In 2000, the share of parents accumulating PLUS debt over $100,000 was only 0.4 percent, but by 2014 the proportion had grown to nearly 4 percent.19 Nearly a third of all dollars in default are held by borrowers with balances over $50,000.20

A previous version of this section stated that almost two in five undergraduates' intergenerational debt is $38,000, it has been updated to reflect one in five dependent undergraduates' intergenerational debt is $38,000.

Citations

- Awilda Rodriguez, a professor at the University of Michiganās School of Education, also has used NPSAS and BPS data to look at racial differences, particularly for Black families, in PLUS loan borrowing from 2000. Her analysis looks at borrowing rates within specific race/ethnicities and by a variety of other demographics including income and marital status. While the Ā鶹¹ū¶³“«Ć½ analysis focuses on the demographics of children of PLUS loan borrowers themselves, Rodriguezās analysis is an important piece of the small body of work done on PLUS loans. To read Rodriguezās analysis in full see Awilda Rodriguez, āUnderstanding the Parent PLUS Loan Debate in the Context of Black Families,ā Research in Race and Ethnic Relations 19 (2015): 147ā170.

- For full methodology and related tables, see Appendices A and B.

- Adjusted Gross Income is used as opposed to gross income because AGI is used on the Free Application for Federal Student Aid (FAFSA) to determine federal financial aid receipt. It is always difficult to determine where exactly to make income cuts, as there is no true definition for low-, middle-, and upper-income families. For this reason, income bands are the same ones used in the U.S. Department of Educationās College Navigator tool to report net price, the price of college after grants are taken into account. The bands are meant to help distinguish among low-, moderate-, middle-, upper-middle-, and upper-income borrowers.

- EFC is a measure established in law that tries to determine a familyās ability to pay for college. While imperfect, it takes into account a familyās taxed and untaxed income, some assets, and government benefits such as Social Security and receipt of food stamps. It is adjusted based on family size and how many children are currently in college. If a family has a zero EFC, for example, the government has determined that the family should not be expected to pay for higher education and the child is eligible for a full Pell Grant, the largest financial aid program for low-income students. The bands chosen for this analysis were suggested by the U.S. Department of Educationās PowerStats tool. For more see .

- Andy Thomasson, āMartin OāMalley has $340,000 in Parent PLUS Loans,ā Chronicle of Higher Education, July 8, 2015, .

- For more analysis of sector by lower- and upper-income and race see tables in Appendix A.

- An analysis of award letters by Ā鶹¹ū¶³“«Ć½ and the nonprofit uAspire that explores this notion further will be released in June 2018. For now, see Rachel Fishman, Kim Dancy, Ben Barrett, and Sophie Nguyen, āShining a Light on Award Letters that Keep Students in the Dark,ā Ed Central (blog), Ā鶹¹ū¶³“«Ć½, January 18, 2018, source.

- Diane Cheng, Debbie Cochrane, and Veronica Gonzalez, Student Debt and the Class of 2016 (Washington, DC: The Institute for College Access and Success, 2017).

- For methodology and tables please see Appendix B.

- Since NPSAS contains student-level data, the intergenerational debt may be understated because there could be mulitple children within a household whose parent has borrowed PLUS.

- Aissa Canchola and Seth Frontman, āThe Significant Impact of Student Debt on Communities of Color,ā CFPB (blog), September 15, 2016, .

- Ben Miller, New Federal Data Show a Student Loan Crisis for African American Borrowers (Washington, DC: Center for American Progress, 2017).

- Ibid.

- Ibid.

- Judith Scott-Clayton, The Looming Student Loan Default Crisis is Worse Than We Thought. (Washington: DC: Brookings Institution, January 10, 2018).

- Ibid.

- Adam Looney and Constantine Yannelis, Borrowers with Large Balances: Rising Student Debt and Falling Repayment Rates (Washington, DC: The Brookings Institution, 2018).

- Ibid.

- Ibid.

- Ibid.

Part II: Racial Wealth Disparities and the PLUS Loan āFixā

Racial Wealth Disparities

How did the Parent PLUS program end up serving exactly who it was meant to for white families but not families of color, especially Black families? The reason is rooted in the racial wealth gap. If the racial income gap runs deep in this country, wealth disparityāor a familyās net worth including all assets and subtracting all liabilitiesāruns even deeper. Since the 1980s, the wealth of white families has grown at three times the rate of Black families.1 If wealth accumulation continues at the same rate over the next 30 years, the wealth of white households will increase by $18,000 per year while for Black families it will only increase by $750 per year.2 Families with less wealth must rely on debt to finance higher education, which in turn can inhibit wealth building.

There are many places where the story of the racial wealth gap begins; crucially, the founding of America allowed for state-sanctioned slavery of Africans. But for the purposes of this story, one that involves higher education and student debt, let us start with the piece of legislation that led to the dramatic expansion and establishment of the system of higher education we are familiar with today: the Servicemanās Readjustment Act of 1944, or the G.I. Bill.

After World War II, millions of working-aged veterans returned to America and to a growing and rapidly changing economy. The passage of the G.I. Bill was meant to help these veterans secure low-cost loans to buy houses and pursue education to help them land jobs. Yet even though the bill is widely credited with greatly expanding Americaās middle class, in implementation the benefits were disproportionately extended to white veterans over Black. This was true for the distribution of higher education benefits but was especially the case when it came to extending mortgages.

Home ownership is one of the driving forces of the racial wealth gap, and it is, in part, rooted in the G.I. Bill. Even though it was race neutral on its faceāindeed, it was the first explicitly race neutral social federal legislation3āBlack veterans were excluded from one of its most important components: the ability to buy a house. White veterans used the guaranteed housing loans to buy houses in fast growing suburbs.4 With that enormous growth in suburbia came the increase in home values in those communities, creating a plum asset for white families to fall back on in times of economic trouble. Black veterans, for the most part, were unable to use these housing benefits because mortgage lenders would not lend to those seeking to purchase homes in Black neighborhoods.5

That Black veterans were unable to access mortgages stems from the establishment of the Federal Housing Administration (FHA) in 1934, 10 years before the passage of the G.I. Bill. Through a practice known as āredlining,ā the FHA and other actors were able to mark neighborhoods of color, especially Black neighborhoods, as bad credit risks, discouraging lending in these neighborhoods and preventing Black homebuyers from buying in white neighborhoods.6 For nearly 30 years, and even with the ārace neutralā G.I. Bill on the books, only 2 percent of FHA loans went to families of color.7 Redlining was outlawed by 1968, but the damage was done. The same residential segregation patterns persist. According to the Dallas Federal Reserve, for example, families with low incomes and subprime credit scores in Dallas today align with the same neighborhoods that were once redlined.8 These areas on average have mortgage delinquency rates of over 30 percent.9

Years of discriminatory housing and lending policies, including the recent subprime mortgage lending crisis and the fallout from the Great Recession, have contributed to wide disparity in who owns a home. Today, 41 percent of Black households own their own homes, compared to 71 percent of white households.10 Even among Black households who do own homes, stark differences remain. Black homeowners are more likely than their white peers to be underwater with their mortgages or have negative equity.11

Owning a home is a building block in the wealth equation for Americans. For many, having a home is an important asset on which to build equity and borrow against for crucial investments such as higher education. Black families cannot tap into home equity like white families can to help pay for higher education because they own homes at lesser rates; recently, they have seen the equity of their homes wiped away in the housing crisis.

Home ownership also can be a resource to draw on during retirement, and a means of transferring wealth to younger generations, in part through inheritance. Most Americans will not receive an inheritance, but this is especially the case for Black households. According to Demos, a public policy organization, while nearly a quarter of white families receive an inheritance, only 11 percent of Black families do.12

"Black families cannot tap into home equity like white families can to help pay for higher education because they own homes at lesser rates; recently, they have seen the equity of their homes wiped away in the housing crisis."

Housing is also critical because of its tie to Kā12 funding structures. Black families often end up in residentially segregated neighborhoods with under-resourced schools. Because home values in those neighborhoods are often lower, less property tax revenue is available to fund the schools. Schools with less money lack the resources necessary to keep class sizes down, hire guidance counselors, and provide other resources necessary to prepare students to enroll in highly regarded colleges. And highly regarded colleges also have the most financial aid to give so that low-income families do not have to go into debt. Even though Brown v. Board of Education made segregation illegal in 1954, in the years that have followed, residential segregation and Kā12 funding structures have returned America to de facto segregation.

While extending mortgages to veterans was the biggest part of the G.I. Bill and likely had the most influence on building Americaās middle class, the higher education benefits in the bill were, in part, another driving factor of the wealth divide. In a growing and changing economy, Black veterans did not have access to the same postsecondary opportunities as white veterans.

Even though the bill was meant to open the doors of postsecondary education to all veterans, Black veterans hoping to take advantage of these benefits often faced Department of Veterans Affairs counselors that shunted them into postsecondary vocational education programs. Only 12 percent of Black veterans went on to college using G.I. Bill benefits, compared to 28 percent of white veterans.13 What is more, Black veterans in the South only had access to a segregated higher-education system with chronically underfunded HBCUs, many of which, according to journalist Edward Humes, were only allowed to provide veterans with limited courses of study.14

By 1947, three years after the passage of the G.I. Bill, increased enrollment had strained colleges and universities, inhibiting access. President Truman assembled a Commission on Higher Education to address broadening access and educating an increasingly diverse student body. Almost as a presage to Americaās current state of higher education, Truman warned, āif the ladder of educational opportunity rises high at the doors of some youth and scarcely rises at the doors of others, while at the same time formal education is made a prerequisite to occupational and social advance, then education may become the means, not of eliminating race and class distinctions, but of deepening and solidifying them.ā15

Since the end of World War II and the rapid growth of computing technologies and artificial intelligence, Americaās economy changed to require new skill sets in the labor market. Higher education became increasingly necessary not just for veterans, but for many others, including women and minority students who previously did not attend higher education in large numbers.16 To help provide the funds necessary for students to access higher education, President Johnson signed the first Higher Education Act (HEA) into law in 1965, an expansion of the federal role in higher-education lending that had begun with the National Defense Education Act of 1958. This role has grown as the price of higher education has increased enormously and states have begun pulling back from funding higher education.

For years now, Americaās system of higher education has not worked for students. Increasingly, higher education is a prerequisite for a well-paying job and in response, students have flooded the campuses of colleges and universities. In 1947, 2.3 million students were enrolled in higher education. Now, it is estimated that 20.9 million enroll.17 Meanwhile, price climbs faster than the rate of inflation, and states, particularly over the last two decades, have disinvested from their institutions of higher education. In 2017, for the first time ever, most states primarily relied on tuition revenue to fund their public colleges and universities.18 The Pell Grant, the federal governmentās signature source of aid for low-income students, has not even come close to keeping pace to make up the difference. Instead, the government has turned to a debt-financed model and students are left to pick up the tab.

This debt-financed model has grown over time, just like the enrollments in higher education. In 1966, the first year students could borrow federal student loans under the Higher Education Act, only 330,000 students did so.19 But once the government sponsored the Student Loan Marketing Association (known as Sallie Mae) in 1972, the student loan portfolio grew significantly.20 The passage of the Middle Income Student Assistance Act in 1978, which made loans available to all students regardless of income, and the establishment of PLUS loans in 1980 again increased the numbers of borrowers.21 But even by the late 1980s, student loans were still only a small fraction of the total debt held by 29- to 37-year-olds. However, currently and with the compounding interest and accumulation of debt over decades, higher education debt is approximately $1.4 trillion and counting, second only to mortgage debt.22 The squeeze of that debt is being felt particularly by Black students and families who struggle the most to repay.

It has been 70 years since the Truman commission, and Trumanās prediction has come true.

It is deeply important that students receive education beyond high school, and yet the ladder of educational opportunityāaccess to high-quality, affordable colleges and universitiesāstops short for many students, especially students of color. As higher education has become increasingly debt-financed, Black families have been caught flat-footed because debt is inextricably tied up with wealth and wealth is inextricably tied up in assets that, through a series of policy decisions, are more likely to be held by white families.

"It has been 70 years since the Truman commission, and Trumanās prediction has come true. It is deeply important that students receive education beyond high school, and yet the ladder of educational opportunityāaccess to high-quality, affordable colleges and universitiesāstops short for many students, especially students of color."

Residentially segregated Kā12 systems frequently feed into under-resourced and low-quality higher education systems. Almost seven out of 10 undergraduates in 2011ā12 attended college 30 miles or less from home, meaning college students are often place-bound and do not go far from where they grew up to attend college.23 The higher education opportunities for low-income Black students who live in segregated areas likely amount to underfunded community colleges and public regional comprehensive four-year institutions and expensive for-profit institutions.

For years now, students have been feeling the sting of state disinvestment from public colleges and universities. For the institutions that serve Black students, the funding has always been unequal, with state disinvestment exacerbating the inequity. For example, after decades of court cases to try and solve unequal funding problems in its higher education system, Mississippiās HBCUs received a $500 million settlement in 2002 that arguably does not go far enough to undo the damage of decades of constrained budgets.24 In 2017 in Maryland, the courts sided with Black colleges that have been fighting the state for more than a decade. A judge in that case ruled that the state must establish new, unique, and high-demand programs at Marylandās public HBCUs.25 An Education Department spokesperson told the Chronicle of Higher Education in 2018 that six states have not proved that they have desegregated their higher education systems. These states are: Florida, Maryland, Ohio, Oklahoma, Pennsylvania, and Texas.26 In total, these states account for 29 percent of Black undergraduate enrollments in the public sector nationwide.27 HBCUs, many of them public, make up less than 5 percent of the total colleges in the U.S. but account for 17 percent of Black graduates.28

In addition to the funding issues that drive prices up at the public colleges where students of color are likely to attend, enrollment in the for-profit sector also contributes to reliance on education debt and an inability to repay. Besides HBCUs, for-profit colleges were also disproportionately affected by the 2011 Parent PLUS loan policy changes. For-profit colleges prey on students of color; many saddle their students with debt in exchange for no degree or degrees with low labor-market returns. For-profit institutions draw Black youth to attend short-term programs with low returns by advertising these programs as a fast and direct path to the workforce and to making money.29

The last part of the wealth equation, one that in todayās economy hinges on access to higher education, is the ability to secure a job with good wages that also comes with important asset-building benefits. Graduates of color are more likely to enter the labor market with student debt and face job discrimination that results in lower wages and less ability to repay those debts. According to Demos, compared to white workers, Black workers are often paid less, hold jobs that fail to provide benefits and protections such as retirement and employer-based healthcare, and experience higher unemployment rates.30

Among the college educated, in part due to an inability to accumulate and transfer wealth through generations and labor-market discrimination, racial economic inequality is at its greatest.31 Black male college graduates, for example, make approximately 75 percent of the wages of white male college graduates.32

Just as higher education has shifted the financial burden to students and families paying the majority of the associated costs, so has the shift from defined-benefit pensions to employer-sponsored plans shifted the burden to workers to save and fund their own retirements. This is leading to a growing retirement crisis for Americans, but more for Black employees than white. According to Nari Rhee from the National Institute of Retirement Security, three out of every five white employees works for an employer that sponsors a retirement plan, whereas only approximately half of Black employees do.33 Even when offered participation in a plan, lower-income groups either cannot contribute or only contribute small amounts that they often withdraw with enormous penalty, to cover financial emergencies.34

"Among the college educated, in part due to an inability to accumulate and transfer wealth through generations and labor-market discrimination, racial economic inequality is at its greatest."

Those unable to save for retirement will be fully reliant on Social Security and other public assistance benefits. Approximately one third of Black single seniors rely entirely on Social Security in retirement, with an average benefit of $1,800 a month in 2011.35 higher-education debt is particularly worrisome for low-income parents who are not far from retirement and who will likely rely on Social Security benefits. The government can and will garnish Social Security paymentsāa modest sum that leaves seniors on the edge of povertyāin order to collect on delinquent Parent PLUS loans. According to a Government Accountability Office report, in fiscal year 2015, approximately 7,339 Parent PLUS borrowers ages 65 and older were currently in default and experiencing government collection methods such as Social Security offsets and seizure of tax refunds.36 In 2005, it was only 2,302 borrowers. That is a 219 percent increase over 10 years.37

Citations

- Dedrick Asante-Muhammad, Chuck Collins, Josh Hoxie, and Emanuel Nieves, The Ever-Growing Gap: Without Change, African-American and Latino Families Wonāt Match White Wealth for Centuries, (Washington, DC: CFED and the Institute for Policy Studies, 2016).

- Ibid.

- Edward Humes, āHow the GI Bill Shunted Blacks into Vocational Training,ā The Journal of Blacks in Higher Education 53 (2006): 92ā104.

- David Callahan, āHow the GI Bill Left Out African Americans,ā Policyshop, November 11, 2013, .

- Ibid.

- Laura Sullivan, Tatjana Meschede, Lars Dietrich, Thomas Shapiro, Amy Traub, Catherine Ruetschlin, and Tamara Draut, The Racial Wealth Gap: Why Policy Matters (New York: Demos and the Institute for Assets & Social Policy at Brandeis University: 2015).

- Ibid.

- Emily Ryder Perlmeter and Garrett Groves, Consumer Credit Trends for Dallas County (Dallas, TX: Federal Reserve Bank of Dallas, 2018).

- Ibid.

- Dedrick Asante-Muhammad, Chuck Collins, Josh Hoxie, and Emanuel Nieves, The Ever-Growing Gap: Without Change, African-American and Latino Families Wonāt Match White Wealth for Centuries, (Washington, DC: CFED and the Institute for Policy Studies, 2016).

- Fenaba R. Addo, Jason N. Houle, Daniel Simon, āYoung, Black, and (Still) in the Red: Parental Wealth, Race, and Student Loan Debt,ā Race and Social Problems 8 (March 2016): 64ā76.

- Laura Sullivan, Tatjana Meschede, Lars Dietrich, Thomas Shapiro, Amy Traub, Catherine Ruetschlin, and Tamara Draut, The Racial Wealth Gap: Why Policy Matters (New York: Demos and the Institute for Assets & Social Policy at Brandeis University: 2015).

- Edward Humes, āHow the GI Bill Shunted Blacks into Vocational Training,ā The Journal of Blacks in Higher Education 53 (2006): 92ā104.

- Ibid

- George Frederick Zook, Higher Education for American Democracy, A Report (Washington, DC: U.S. Government Printing Office, 1947).

- Philo A. Hutcheson, āThe Truman Commissionās Vision of the Future,ā Thought & Action (Fall 2007): 107ā115.

- National Center for Education Statistics, āTotal Fall Enrollment in Degree-Granting Postsecondary Institutions, by Attendance Status, Sex of Student, and Control of Institution: Selected Years, 1947 through 2025,ā table, U.S. Department of Education, .

- Sophia Laderman, State Higher Education Finance: FY 2017 (Boulder, CO: SHEEO, 2018), .

- Alisa F. Cunningham and Deborah A. Santiago, Student Aversion to Borrowing: Who Borrows and Who Doesnāt (Washington, DC: Institute for Higher Education Policy and Excelencia in Education, 2008).

- Ibid.

- Ibid.

- Ibid.

- Ā鶹¹ū¶³“«Ć½ analysis of NPSAS 2012 data.

- Adam Harris, āThey Wanted Desegregation. They Settled for Money, and Itās Ā鶹¹ū¶³“«Ć½ to Run Out,ā Chronicle of Higher Education, March 26, 2018, .

- Danielle Douglas-Gabriel, āCourts Side with Maryland HBCUs in Long-Standing Case Over Disparities in State Higher Education Funding,ā Washington Post, November 9, 2017, .

- Ibid.

- Ā鶹¹ū¶³“«Ć½ analysis of U.S. Department of Education IPEDS data for 2016 fall enrollment of degree-seeking undergraduates.

- Adam Harris, āThey Wanted Desegregation. They Settled for Money, and Itās Ā鶹¹ū¶³“«Ć½ to Run Out,ā Chronicle of Higher Education, March 26, 2018, .

- Megan M. Holland and Stefanie DeLuca, āāWhy Wait Years to Become Something?ā Low-Income Youth and the Costly Career Search in For-Profit Trade Schools,ā Sociology of Education 89 (2016): 261ā278.

- Laura Sullivan, Tatjana Meschede, Lars Dietrich, Thomas Shapiro, Amy Traub, Catherine Ruetschlin, and Tamara Draut, The Racial Wealth Gap: Why Policy Matters (New York: Demos and the Institute for Assets & Social Policy at Brandeis University: 2015).

- S. Michael Gaddis, āDiscrimination in the Credential Society: An Audit Study of Race and College Selectivity in the Labor Market,ā Social Forces (2014): 1ā29.

- Bradbury 2002 study as cited in S. Michael Gaddis, āDiscrimination in the Credential Society: An Audit Study of Race and College Selectivity in the Labor Market,ā Social Forces (2014): 1ā29.

- Nari Rhee, Race and Retirement Insecurity in the United States (Washington, DC: National Institute on Retirement Security, 2013).

- Serena Lei, āNine Charts Ā鶹¹ū¶³“«Ć½ Wealth Inequality in America (Updated),ā The Urban Institute, October 5, 2017, .

- Thomas M. Shapiro, Toxic Inequality: How Americaās Wealth Gap Destroys Mobility, Deepens the Racial Divide, & Threatens our Future (New York: Basic Books, 2017).

- Social Security Offsets: Improvement to Program Design Could Better Assist Older Student Loan Borrowers with Obtaining Permitted Relief, GAO 17-45 (Washington, DC: U.S. Government Accountability Office, 2016).

- Ibid.

Part III: The PLUS Loan āFixā

Given the massive evidence of state-sponsored discrimination and resulting wealth disparities, all leading to low-income Black households being disproportionately burdened by Parent PLUS loans, what did Congress and the federal government do? It did essentially nothing. And so the problem continues to grow.

In 2013ā14, when the Education Department revisited the Parent PLUS regulations, the adverse credit history check was one of the issues different stakeholders, including colleges and universities, student groups, and consumer advocates, tried to fix. Though the Department did not have the legal standing to revert completely to the pre-2011 credit standard, it came up with a middle-ground solution that instituted a de minimus amount to the check. In this case, total debts with adverse conditions such as 90-day delinquency must be over $2,085 (pegged to inflation in 2015). This resulted in an overall slightly weakened regulation compared with what had been the standard.

This compromise was hardly satisfying to those involved. On the one side, HBCUs had already experienced huge losses of revenue and students. On the other, consumer advocates remained concerned that low-income parents were still being offered loans when they had no ability to repay them, with powerful governmental collection tactics, such as garnishing Social Security and seizing tax refunds, looming in the background.

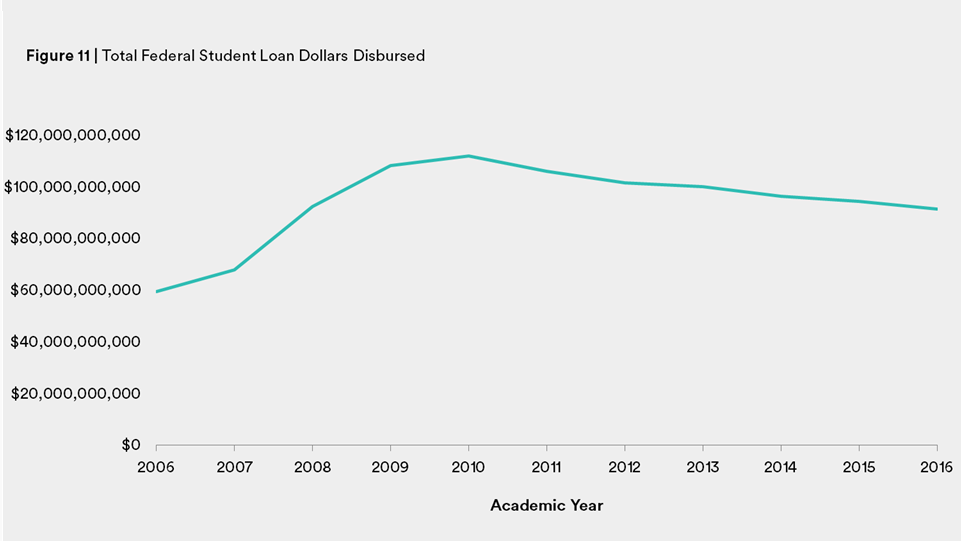

Despite these significant issues, Parent PLUS loan borrowing has increased even while all other federal student loans have been decreasing, except for Graduate PLUS loans. According to Education Department disbursement and recipient data, over the past decade there has been enormous fluctuation and growth in the federal student loan program.1 In academic year 2006ā07, $59.6 billion in federal education loans were disbursed (See Figure 11). This includes subsidized, unsubsidized, Parent PLUS, and Grad PLUS loans. The disbursements hit an all-time high at $111.9 billion in 2010ā11, which was both the height of the Great Recession and, for largely demographic reasons, the year when student enrollments peaked. As the economy recovered and enrollment declined, total yearly loan disbursements have fallen every year. In the most recent year of available data, academic year 2016ā17, the total was $91.3 billion.

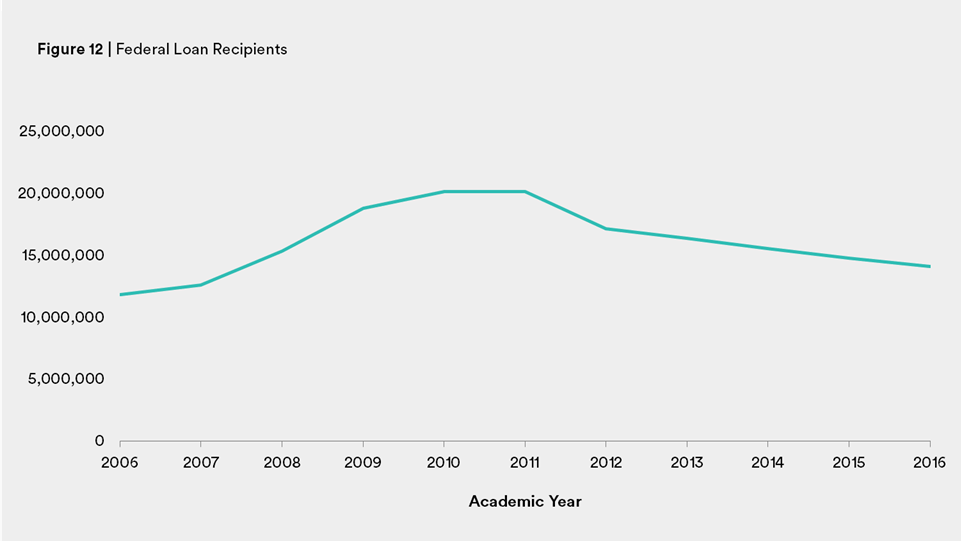

In terms of loan recipients, the pattern has been similar. In 2006ā07, there were 11.8 million federal education loan recipients (See Figure 12). Recipients peaked during 2011ā12, at 20.1 million borrowers. In 2016ā17, that number fell to 14.1 million recipients.

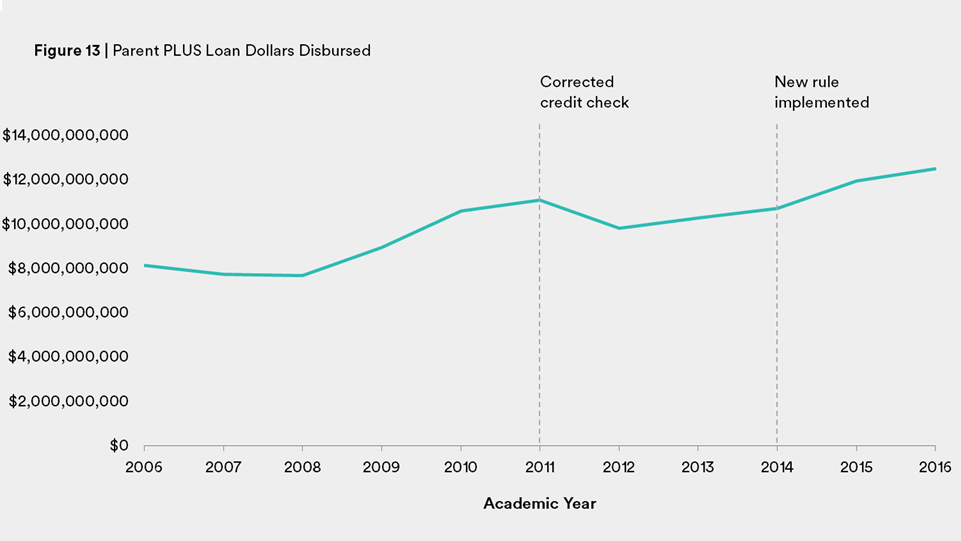

Yet during the same period, Parent PLUS loans have grown in terms of yearly disbursals. In 2006ā07, $11.1 billion in Parent PLUS loans were disbursed (See Figure 13). After the Department made the credit change, the disbursal fell to $9.8 billion in 2012ā13. But once the new rule was implemented in 2014ā15, the yearly disbursals recovered. Last year, Parent PLUS loans experienced their highest yearly disbursement yet, $12.4 billion.

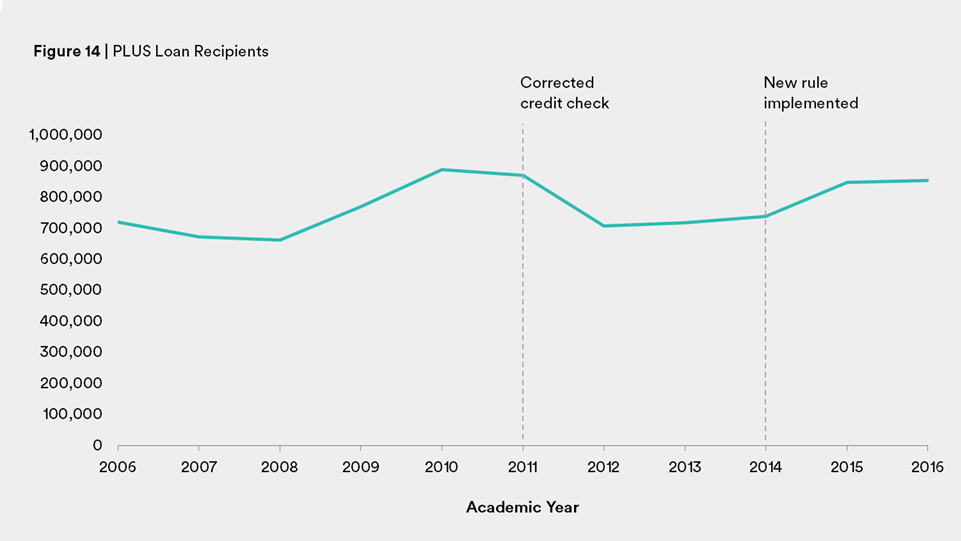

The number of Parent PLUS recipients has followed a similar pattern to that of all student loans, though the decline in recipients has not been as steep. In 2006ā07, there were approximately 720,000 Parent PLUS recipients (See Figure 14). In the lead up to the credit check change in 2011ā12, there were about 870,000 recipients. One year later, after the Department changed the credit check, there was a decline to approximately 707,000 recipients. Since the new credit check regulation has been implemented, the number of recipients has largely recovered and stands at 854,000.

Since the new check was put into place, Parent PLUS loan volume in terms of dollars has more than recovered. While there is still a slight difference in the number of recipients pre- and post-credit check, higher education enrollments have been declining slightly since the height of the recession, which may help explain the downward trend.

Citations

- All disbursement and recipient data were gathered using Ā鶹¹ū¶³“«Ć½ās Higher Ed Index, which uses U.S. Department of Education Federal Student Aid data. For more information see .

Policy Recommendations

The PLUS loan credit check āfixā has allowed the program to come roaring back to life with little oversight and little to ensure families are not borrowing more than they can hope to repay. These loans put a parentās future at risk, reduce the opportunity to build wealth and retirement security, and weaken the investment his or her children will see from a degree. There are so many policies that need to be addressed in order to help narrow the racial wealth gap in the U.S. Fixing the Parent PLUS loan and other changes to higher education policy are just small changes in a series of larger steps that local, state, and federal government must take to rectify racial wealth disparity.

Right now, the federal government provides āaccessā to higher education, via PLUS loans, to any college or university as long as a parent is approved. But if the parent is low-wealth, then a PLUS loan does not provide true access because it will ultimately result in harm and erasure of wealth when the bill is due. The switch to intergenerational debt-financing for higher education has worsened the racial wealth divide. The federal governmentās role in higher education is important, and it already provides grants and loans to help students afford it, but that is not enough. In order to provide true access for low-wealth families, there must be a targeted investment that is not debt-financed and will completely bring down the cost of, at a minimum, public two- and four-year universities while holding institutions accountable for that investment.

There are several interim policy goals that Congress could address now with the program that will put it on firmer footing and end what are often predatory lending practices. But just fixing the Parent PLUS loan program does not even begin to address the inequality faced by Black families when it comes to accessing affordable, high-quality higher education that leads to degrees of value. That outcome requires long-term policy with strategies to promote reduction of debt and an affordable higher education to Black students and other historically disadvantaged students of color.

Interim PLUS Loan Policy Fixes

1) Preserve PLUS but Add an āAbility-to-Payā Measure Using EFC. It might be tempting to end the Parent PLUS loan program and let the private market prevail. But turning things over to the private market usually leads to predatory products over time that are worse in terms of consumer protections. Instead, the Parent PLUS program should be preserved for those looking for a fixed-rate higher-education loan with stronger consumer protections.

Looking at a parentās adverse credit history is not the only way to accurately assess whether or not someone has the ability to repay the loan. Someone with no income, no assets, and no credit history would be Parent PLUS-eligible, because that person does not have a bad credit history. Adding an ability-to-repay measure to the Parent PLUS credit check would be a much fairer standard, ensuring that parents are able to access a loan that is capped to prevent borrowing beyond their means. The government already collects information on a familyās ability to repay through the FAFSA and its calculation of expected family contribution. EFC could be used in tandem with adverse credit history to determine a familyās loan limit. If a family has a zero EFC, the parent applying for a PLUS loan would not be extended one. Instead, the student would be offered additional loans up to the independent lending limit, a process that currently happens when parents are rejected for PLUS loans based on adverse credit history alone. In other words, if a parent applies for a PLUS loan with EFC of zero to $4,000 or $5,000 depending on the year a student is in school, his child would instead be given access to $4,000 to $5,000 in federal student loans. Overall, Parent PLUS Loan limits would vary and be capped by EFC or COA, whichever is lower.

While it may be unsatisfactory to give more loans to low-income students, the loans made directly to students come with more protections than Parent PLUS loans, like access to income-driven repayment and lower interest rates. They also ensure the neediest of parents do not end up with non-dischargeable debt as they close in on retirement. Students should also be required to exhaust their own loan eligibility before their parents turn to PLUS.

Box 3

The PROSPER Act and Capping PLUS: Misdirected Idea

Republicans of the House Committee on Education and the Workforce unveiled their reauthorization of the Higher Education Act in December 2017. The Promoting Real Opportunity, Success and Prosperity through Education Reform, or PROSPER, Act sets out to cap parent loans at $12,500 per student per year, with a $56,250 lifetime cap. While capping the loan will certainly prevent parents from accumulating large amounts of debt, it still will not solve the issue that low-income families face: any amount of parental debt is detrimental to their financial well-being. An ability-to-pay metric as discussed above would be a more sensible natural cap based on real financial data.

2) Prevent Institutions from Listing PLUS Loan Amounts in Financial Aid Award Letters. Once students are accepted into college, they receive a financial aid award letter detailing what federal, state, local, and institutional aid for which they are eligible. An analysis by Ā鶹¹ū¶³“«Ć½ and uAspire of thousands of award letters to predominantly low-income families revealed that 17 percent of letters contained PLUS loans.1 A Parent PLUS loan amount should never be packaged anywhere within a studentās financial aid award letter as it is not a guarantee and is not direct aid to the student. Institutions should be encouraged to adopt the Education Departmentās Financial Aid Shopping Sheet as their aid letter or at a minimum only mention Parent PLUS loans as a way to cover outstanding expenses along with other options, with no amount given.

3) Require Entrance Counseling and Better Disclosure Surrounding Terms and Conditions of PLUS Loans. Entrance counseling is required of all federal student loan borrowers but cannot be required for Parent PLUS borrowers. The only counseling requirement currently mandatory for Parent PLUS borrowers is when a parent is rejected but wins an appeal. Going forward, Congress should make all federal higher-education loans align with current entrance counseling requirements. Parent PLUS entrance counseling must indicate that the loan is borrowed by the parent, is non-transferrable to the student, and is not eligible for income-driven repayment plans. It must also explain repayment options, including deferments and forbearances, and that the loan is not dischargeable in bankruptcy. Finally, it should clearly state that failure to pay not only results in damage to credit scores but could also result in wage garnishment, Social Security offsets, and seizure of tax refunds.

4) Collect Better Data on PLUS Loans. The Education Department should release more detailed information on PLUS loans, broken out by loan type. As research in this report has shown, the only way to understand the demographics of PLUS loan borrowers currently is through triangulation using U.S. Department of Education surveys of students. The lack of default data makes it almost impossible to determine whether PLUS loans are predatory. The problems with PLUS loan data are twofold: 1) Parent PLUS and Graduate PLUS, federal loans made for graduate education, are often combined even though the demographics of borrowers are different; and 2) Parent PLUS loan data are not reported and sometimes not even collected. Right now, policymakers are operating blind when it comes to understanding and diagnosing problems with the PLUS loan portfolio. In the aggregate the portfolio performs well, but even with the limited data available there are worrisome issues with PLUS. Without better information, it is difficult to craft thoughtful solutions. The Education Department should release the following data by institutions, sector, and portfolio, separated by Grad and Parent PLUS: lifetime (20- or 30-year) default rates; cohort-default rates; PLUS loan repayment outcomes including delinquency, by income and race; data to calculate accurate repayment rates; and data to calculate total familial indebtedness by linking PLUS and undergraduate debt.

5) Hold Colleges Accountable for Parent PLUS Default Rates. Parent PLUS loans are not included in institutional cohort default rate calculations, making them a no-strings-attached revenue source for colleges and universities. Colleges and universities should face the same accountability for these loans as subsidized and unsubsidized direct loans. Three-year institutional cohort default rates should be calculated for Parent PLUS. Just like with current cohort default rate policy, institutions should face sanctions if their Parent PLUS default rate is at least 30 percent (if not lower, since parents must pass a credit check), including loss of eligibility to offer PLUS loans if the rate remains high year over year.

6) Allow Parent PLUS Loans to be Dischargeable in Bankruptcy. Higher education loans, whether federal or private, are not usually dischargeable in bankruptcy. While private higher-education loans should be dischargeable like other consumer debts, federal loans will likely remain nondischargeable as they are backed by taxpayer dollars. The Trump administration put out a call for comment on what the government should do when evaluating whether student loans should be discharged in bankruptcy. It is promising that the administration is exploring ways in which to simplify the process for getting loans discharged. Given that there are hardly any safety valves for Parent PLUS debt, and that of all loans within the federal portfolio of higher-education loans it most closely mimics private debt, the path to discharging PLUS debt should have a simpler test compared to current standards. In the future, Congress should make PLUS loans dischargeable in bankruptcy, especially because it already has some underwriting, given the adverse credit history check, and even more so once an ability-to-pay measure is added to the credit check.

7) Improve Parent PLUS Loan Servicing. There are very few relief mechanisms for Parent PLUS debt other than deferment, forbearance, graduated repayment plans, and consolidation. Servicers working with Parent PLUS borrowers who struggle to repay must explain deferment and forbearance options along with federal consolidation options, especially if the borrower has exhausted her hardship deferments or said that her financial situation is unlikely to change. If a PLUS borrower has large PLUS debt, consolidating will stretch out monthly payments over a longer time, meaning a lower monthly payment. And, servicers should explain, in many situations consolidation into a direct consolidation loan will allow PLUS borrowers to access Income-Contingent Repayment.

Long-Term Policy Goals

8) Promote āRace Consciousā or āTargeted Universalismā Financial Aid Policies. It is clear that current higher education policies exacerbate the racial wealth gap. Because the risk of debt is much higher for students of color, especially Black students, every attempt must be made to reduce the price of a college education on the front end either through direct grant aid (for example, a double Pell Grant for students of color with zero EFC) or aid to institutions that predominantly serve those populations. It is hard to conceive what a program such as this would look like, but it would have to be a large investment of money specifically to help students of color, primarily Black students and other groups such as American Indians, who are often masked in outcomes data due to their small population. This money could come from the tens of billions of dollars that are allocated for higher education benefits in our tax code that overwhelmingly benefit wealthy families.2

This aid could be need-based but given how wide the racial wealth gap is, an argument could be made to make it non-need-based. The only stipulation on this aid would be that it not be available to the for-profit sector, which has had poor outcomes with students of color. And the answer should not be to leave price reduction and aid distribution to states alone. In the past, as seen with the state implementation of the G.I. Bill, biases led to unequal distribution of benefits to veterans of color. For this reason, there would have to be a strong federal and state partnership in place to distribute that aid and make debt-free college a reality for students of color.

9) Hold Institutions Accountable. There is very little accountability in federal higher education policy, letting billions of taxpayer dollars flow to institutions, including taxpayer-backed higher-education loans that have the potential to leave some students worse off than if they had never enrolled. Ā鶹¹ū¶³“«Ć½ has previously discussed accountability measures in Starting From Scratch: A New Federal State Partnership for Higher Education.3 These measures have two goals: 1) to ensure that public dollars are well targeted; and 2) to help students and families make well-informed decisions about their educational investments.

Accountability metrics, peer groups, and sanctions should be developed in consultation with relevant stakeholders including colleges and universities, their membership organizations, accreditors, federal and state policymakers, and student groups. At a minimum, these metrics must focus on the number and percentage of students who progress through their programs in a timely fashion, graduate or successfully transfer to the next step in an educational track, and secure employment that pays a family-sustaining wage after leaving college. These data would need to be collected at the student level and would require Congress to authorize a Student Level Data Network. This would allow data to be disaggregated by various demographics at the institutional, programmatic, and student level.

10) Keep Strong Regulation of the For-Profit Sector in Place. Under the Trump administration and a Republican Congress, moves have been made to undo critical regulations and laws meant to reign in an industry that often leaves students, especially Black students, degreeless and in debt. From the Education Department rewriting the Gainful Employment regulation, to the PROSPER Act rescinding a rule that would allow for-profit colleges and universities to receive up to 100 percent of their revenue through taxpayer dollars, to allowing Pell Grants for short-term programs that will not prepare students for a career, the renewed traction of the for-profit industry is a move in the wrong direction for students and taxpayers. Strong laws and regulation of for-profit higher education is essential to prevent harm to students and prevent waste of taxpayer dollars.

11) End Legacy Admissions and Other Preferences that Correlate with Wealth. Although most students attend open-access or less-selective higher-education institutions such as community colleges and regional public and private institutions, many low-income students are shut out from highly selective colleges and universities. When low-income students are able to enroll in selective higher-education institutions, they fare as well as their wealthier peers and often receive more resources and monetary support from the institution.4

Low-income students of color who are academically qualified should have the opportunity to attend a prestigious college or university without going through a cumbersome and opaque admissions and financial aid process. For this reason, the most highly resourced and highly selective institutions should end legacy admissions and other preferential admissions treatment that overwhelmingly favor wealthy and white families, including early decision programs.5

12) Allow for Targeted Loan Cancellation and Preserve Public Service Loan Forgiveness. As shown in this report, many Black student loan borrowers, even those who have bachelorās degrees, struggle to repay their debt years later. Many fall delinquent or default on their loans. A renewed investment into Black students as called for in this paper will reduce, or perhaps even do away with, borrowing for these students. But for those borrowers currently in the system, struggling with debt and facing labor market discrimination and/or degrees with little value, there must be a way to cancel debt sooner than signing up for an IDR plan and waiting 20 to 25 years for forgiveness while interest accrues. Those who fall delinquent on their loans should be able to have their debts canceled if, for example, they have received a means-tested federal benefit such as enrollment in Medicaid, Supplemental Security Income (SSI), or Supplemental Nutrition Assistance Program (SNAP) for a determined number of consecutive years of repayment.

Additionally, given that Black college-educated workers are overrepresented in federal and state government, preserving Public Service Loan Forgiveness (PSLF) is important for narrowing the racial wealth gap.6 This program allows borrowers in IDR plans who make 10 years of on-time payments, and who work full time for the government or a nonprofit to have their loans forgiven.

Citations

- Forthcoming report to be published from Ā鶹¹ū¶³“«Ć½ and uAspire in June 2018.

- Ā鶹¹ū¶³“«Ć½ās Higher Education Initiative has written about redirecting the more than $180 billion in tuition tax breaks, tax advantaged savings plans, and the student loan interest deduction to the Pell Grant program. See Stephen Burd, Kevin Carey, Jason Delisle, Rachel Fishman, Alex Holt, Amy Laitinen, and Clare McCann, Rebalancing Resources and Incentives in Federal Student Aid (Washington, DC: Ā鶹¹ū¶³“«Ć½, 2013).

- Ben Barrett, Stephen Burd, Kevin Carey, Kim Dancy, Manuela Ekowo, Rachel Fishman, Alexander Holt, Amy Laitinen, Mary Alice McCarthy, and Iris Palmer, Starting from Scratch: A New Federal and State Partnership in Higher Education (Washington, DC: Ā鶹¹ū¶³“«Ć½, 2016).

- Stephen Burd, ed., Moving on Up? What a Groundbreaking Study Tells Us Ā鶹¹ū¶³“«Ć½ Access, Success, and Mobility in Higher Education (Washington, DC: Ā鶹¹ū¶³“«Ć½, October 2017).

- Harold Levy and Peg Tyre, āHow to Level the College Playing Field,ā New York Times, April 7, 2018, .

- Forthcoming research from Kim Dancy to be published summer 2018 at Ā鶹¹ū¶³“«Ć½.

Selected Bibliography

Addo, Fenaba R., Jason N. Houle, and Daniel Simon, āYoung, Black, and (Still) in the Red: Parental Wealth, Race, and Student Loan Debt.ā Race and Social Problems 8 (March 2016): 64ā76.

Armantier, Olivier, Luis Armona, Giacomo De Giorgi, and Wilbert van der Klaauw. Which Households Have Negative Wealth? New York: Federal Reserve Bank of New York, 2016.

Asante-Muhammad, Dedrick, Chuck Collins, Josh Hoxie, and Emanuel Nieves. The Ever-Growing Gap: Without Change, African-American and Latino Families Wonāt Match White Wealth for Centuries. Washington, DC: CFED and the Institute for Policy Studies, 2016.

Barrett, Ben, Stephen Burd, Kevin Carey, Kim Dancy, Manuela Ekowo, Rachel Fishman, Alexander Holt, Amy Laitinen, Mary Alice McCarthy, and Iris Palmer. Starting from Scratch: A New Federal and State Partnership in Higher Education. Washington, DC: Ā鶹¹ū¶³“«Ć½, 2016.

Berman, Jillian. āNew York Fed Warns of Troubling Consequence of Rising Student Loan Debt.ā Market Watch, August 2, 2016. .

Brown, Carlton. āNegotiated Rulemaking for Higher Education 2013.ā Testimony given at the U.S. Department of Education Office of Postsecondary Education Public Hearing, Atlanta, GA, June 4, 2013.

Burd, Stephen ed. Moving on Up? What a Groundbreaking Study Tells Us Ā鶹¹ū¶³“«Ć½ Access, Success, and Mobility in Higher Education. Washington, DC: Ā鶹¹ū¶³“«Ć½, October 2017.

Burd, Stephen, Kevin Carey, Jason Delisle, Rachel Fishman, Alex Holt, Amy Laitinen, and Clare McCann. Rebalancing Resources and Incentives in Federal Student Aid. Washington, DC: Ā鶹¹ū¶³“«Ć½, 2013.

Callahan, David. āHow the GI Bill Left Out African Americans.ā Policyshop, November 11, 2013. .

Canchola, Aissa, and Seth Frontman. āThe Significant Impact of Student Debt on Communities of Color.ā CFPB [blog], September 15, 2016. .

Cervantes, Angelica, Marlena Cruesere, Robin McMillion, Carla McQueen, Matt Short, Matt Steiner, and Jeff Webster. Opening Doors to the Higher Education Act: Perspectives on the Higher Education Act 40 Years Later. Round Rock, TX: Texas Guaranteed Student Loan Corporation, 2005.

Cheng, Diane, Debbie Cochrane, and Veronica Gonzalez. Student Debt and the Class of 2016. Washington, DC: The Institute for College Access and Success, 2017.

Cunningham, Alisa F., and Deborah A. Santiago. Student Aversion to Borrowing: Who Borrows and Who Doesnāt. Washington, DC: Institute for Higher Education Policy and Excelencia in Education, 2008.

Douglas-Gabriel, Danielle. āCourts Side with Maryland HBCUs in Long-Standing Case Over Disparities in State Higher Education Funding.ā Washington Post, November 9, 2017. .